Sovereignty Insights

France: analysis of foreign dependencies

There is a dangerous misconception in the way governments and businesses view their economies: they think they understand them. They look at macroeconomic aggregates, production figures, employment rates, trade balances, etc., and imagine that this is enough to understand a country's real place in the global system.

There is a dangerous idea in the way states and companies look at their economies: they think they understand them. They look at macroeconomic aggregates, production figures, employment rates, trade balances, and convince themselves this is enough to understand a country’s real position in the global system.

It is not.

The truth is much simpler and much more brutal: an economy is nothing but a web of dependencies.

What matters is not what a country produces or sells, but who it depends on to produce, sell, invest, feed itself, and function.

This fundamental reality remains invisible in public statistics.

Yet it is the core of strategic sovereignty: the ability of a country to keep making decisions for itself even as the world around it collapses.

This is exactly what our analysis of the FIGARO (Eurostat) and SIRENE (INSEE) datasets reveals for France in 2023: a clear, quantified, documented assessment of France’s real position in global value chains and the systemic vulnerabilities that come with it.

What we found is simple to summarize: French dependencies run much deeper and are much more invisible than national statistics suggest.

The starting point: understanding the real structure of France

France had 2 419 964 active commercial companies as of December 31, 2023. A massive number that requires context, because behind this total the structure is extremely unbalanced:

83.6% of these companies operate in real estate activities, driven mostly by property holding companies known as SCI.

Manufacturing, the part of the economy that keeps value chains running, represents only 0.05 percent of all companies.

In other words: France does not produce many industrial companies. But it relies massively on the ones that remain.

This gap between real industrial capacity and strategic importance creates a first vulnerability: a handful of highly specialized sectors carry a disproportionate share of the country’s functioning. But the second vulnerability, and a far more serious one, hides in the data on international trade flows.

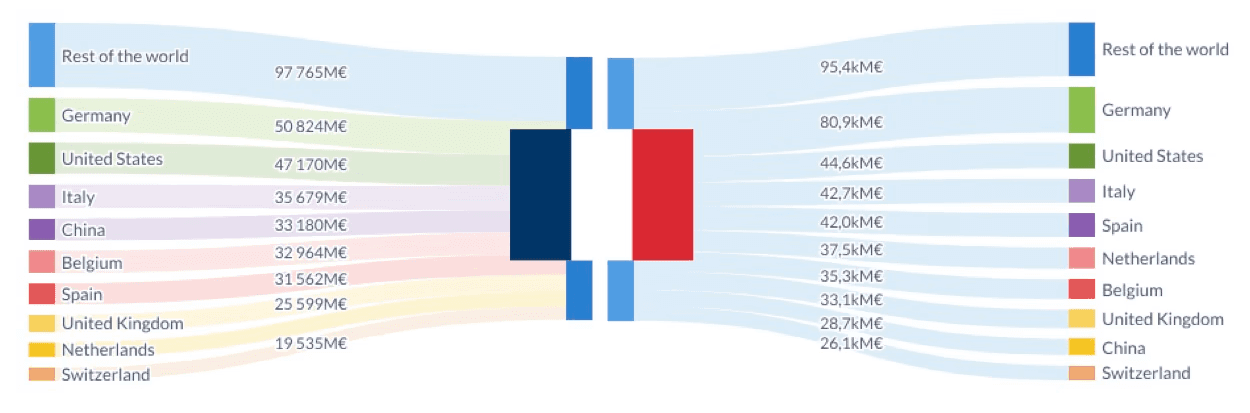

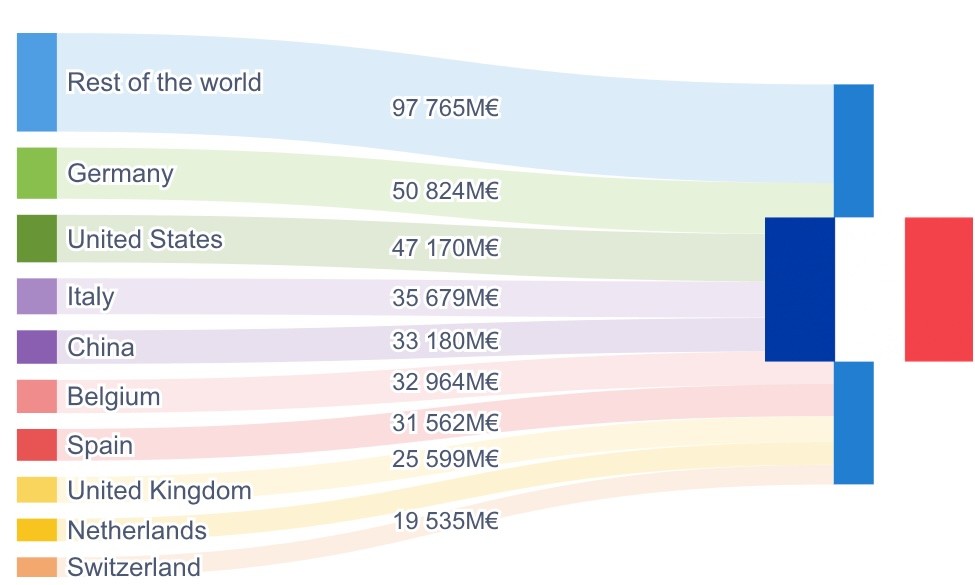

What France buys: 23.5 percent foreign dependency, including an unknown share

In 2023, French companies imported 627.5 billion euros worth of foreign inputs in order to produce. This represents 23.53% of all intermediate purchases. A reasonable figure for a developed country? Not exactly.

The details tell a different story:

France’s main foreign suppliers are:

|

|

But there is a spectacular anomaly in this ranking: France’s top foreign supplier is not a country. It is a statistical blind spot.

FIGW1 ("Rest of the World") is not a region or a geographical area. It is an aggregate of unclassified countries, a global bucket into which tens of billions of euros of flows disappear.

What this means is simple: a significant part of French production depends on actors France is not able to identify. No sovereign state can make good decisions under this level of obscurity.

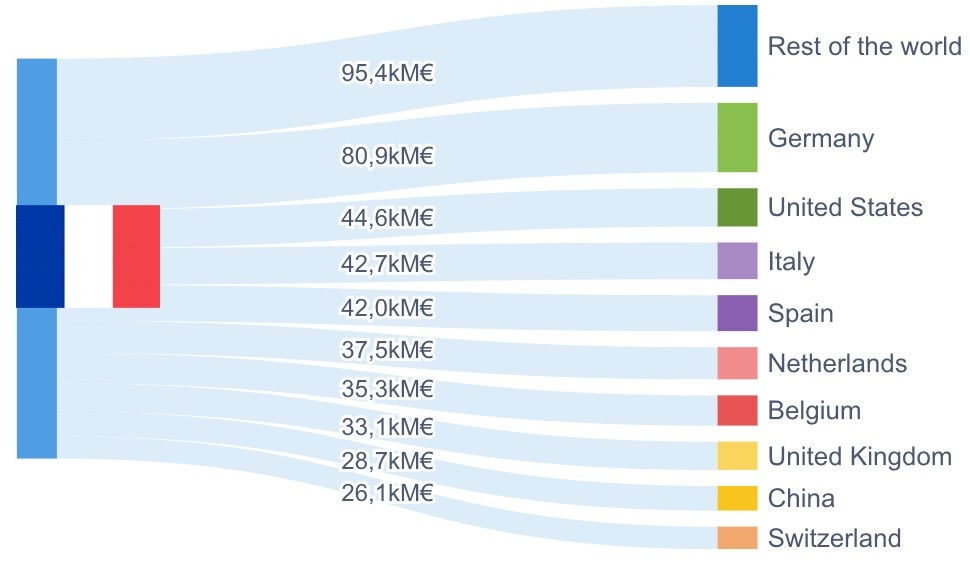

What France sells: high exposure to sensitive geopolitical blocs

On the export side, the diagnosis is no more reassuring. In 2023, 20.64 % of French intermediate production was destined for foreign markets. And once again, the top foreign “client” is FIGW1 with 97.7 billion euros.

Other major clients include:

|

|

But the weight of geopolitically sensitive countries is striking:

🇺🇸United States: 47.17 billion euros

🇨🇳China: 33.18 billion euros

🇹🇷Turkey: 7.89 billion euros

🇷🇺Russia: 5.89 billion euros

🇸🇦Saudi Arabia: 1.88 billion euros

These dependencies are not only economic. They are political, technological, and strategic.

France’s strategic sectors rely on fragile value chains

Sector analysis reveals a major pattern: the sectors that carry France’s industrial sovereignty are also the sectors most exposed to international dependencies.

Most exposed sectors on the purchasing side:

Chemicals

Automotive

Metallurgy

Electronics

Machinery and equipment

Refined petroleum

Energy

Industrial food processing

Most exposed sectors on the sales side:

Aerospace and naval transport

Chemicals

Technology and electronics

Machine tools

Automotive

Defense and public administration

In other words: the sectors that matter the most are also the ones that would be hit the hardest by a geopolitical disruption. And yet, in terms of number of companies, these sectors are extremely small: only about 1200 to 1500 truly strategic companies across the entire country.

The resilience of France relies on them.

Dependencies on sanctioned countries: low in volume, critical in nature

Surprisingly, flows with officially sanctioned OFAC and EU countries are relatively small. Russia accounts for 4.34 billion euros in imports and 5.89 billion euros in exports.

At first glance, nothing alarming. But these flows affect very specific sectors:

metals

chemicals

machine tools

industrial food processing

construction

transport

pharmaceuticals

scientific research

These sectors are tiny in number of actors but central in French industrial value chains. What matters is not the size of the flow. It is the depth of the dependency and the strategic nature of the goods involved.

The systemic risk: the French economy depends on actors it cannot see

The global picture can be summarized as follows:

France depends on foreign actors for 20 to 25% of its ability to function.

A significant part of these dependencies is blurry, poorly documented, or invisible (FIGW1).

The most exposed sectors are also the most strategic.

French sovereignty relies on a very small number of industrial companies.

This is the definition of an unmanaged systemic risk.

France is not only dependent. It is dependent on actors it has not identified, in sectors it does not monitor, across value chains it cannot see beyond the first tier. No country is sovereign under these conditions.

Why this diagnosis matters: strategic sovereignty starts with visibility

France has the capacity to produce, export, and innovate. What it does not have, like all Western countries, is the ability to see its real dependencies. FIGARO provides a macro picture. SIRENE provides a surface-level structure.

But no state today has operational visibility into its value chains:

indirect suppliers

real countries of origin

multi-tier dependencies

geopolitical exposure

risk concentration

vulnerabilities linked to FIGW1

critical companies

potential points of failure

This is not an economic issue. This is a strategic sovereignty issue.

A state cannot protect what it cannot see.

A company cannot anticipate what it does not measure.

An economy cannot withstand what it does not understand.

For France, the first step is not to produce more. It is to make the invisible visible.

This is exactly what Sentinel is designed to achieve

It is not enough to know that 23 percent of purchases come from abroad. You need to know from whom, how, through which chain, through which intermediary, with which geopolitical risks, and with what probability of disruption.

Sentinel was designed for exactly this purpose:

reconstructing real value chains from public, private, and satellite data

automatically identifying critical dependencies

measuring exposure to geopolitical blocs

detecting breaking points across industrial chains

analyzing multi-tier suppliers

assigning sector and national sovereignty scores

allowing decision-makers to see what was previously invisible

Strategic sovereignty is not a slogan. It is an operational capability built on knowledge.

And knowledge starts with one thing: visibility.

In conclusion

This analysis does not tell a story about international trade.

It tells the story of France’s deep dependencies, the ones that define its ability to produce, invest, defend itself, and innovate.

The diagnosis is clear: France depends far more than it believes, and more importantly, it depends on actors it cannot see.

In a world where geopolitics reshapes economic rules, the real question is no longer “How much do we depend on?” but “Are we able to see our dependencies before they turn into ruptures?”

With our Sentinel solution, the answer can finally be yes.

Every week we publish the analysis of a new country on this blog. Sign up for free here.

There is a dangerous idea in the way states and companies look at their economies: they think they understand them. They look at macroeconomic aggregates, production figures, employment rates, trade balances, and convince themselves this is enough to understand a country’s real position in the global system.

It is not.

The truth is much simpler and much more brutal: an economy is nothing but a web of dependencies.

What matters is not what a country produces or sells, but who it depends on to produce, sell, invest, feed itself, and function.

This fundamental reality remains invisible in public statistics.

Yet it is the core of strategic sovereignty: the ability of a country to keep making decisions for itself even as the world around it collapses.

This is exactly what our analysis of the FIGARO (Eurostat) and SIRENE (INSEE) datasets reveals for France in 2023: a clear, quantified, documented assessment of France’s real position in global value chains and the systemic vulnerabilities that come with it.

What we found is simple to summarize: French dependencies run much deeper and are much more invisible than national statistics suggest.

The starting point: understanding the real structure of France

France had 2 419 964 active commercial companies as of December 31, 2023. A massive number that requires context, because behind this total the structure is extremely unbalanced:

83.6% of these companies operate in real estate activities, driven mostly by property holding companies known as SCI.

Manufacturing, the part of the economy that keeps value chains running, represents only 0.05 percent of all companies.

In other words: France does not produce many industrial companies. But it relies massively on the ones that remain.

This gap between real industrial capacity and strategic importance creates a first vulnerability: a handful of highly specialized sectors carry a disproportionate share of the country’s functioning. But the second vulnerability, and a far more serious one, hides in the data on international trade flows.

What France buys: 23.5 percent foreign dependency, including an unknown share

In 2023, French companies imported 627.5 billion euros worth of foreign inputs in order to produce. This represents 23.53% of all intermediate purchases. A reasonable figure for a developed country? Not exactly.

The details tell a different story:

France’s main foreign suppliers are:

|

|

But there is a spectacular anomaly in this ranking: France’s top foreign supplier is not a country. It is a statistical blind spot.

FIGW1 ("Rest of the World") is not a region or a geographical area. It is an aggregate of unclassified countries, a global bucket into which tens of billions of euros of flows disappear.

What this means is simple: a significant part of French production depends on actors France is not able to identify. No sovereign state can make good decisions under this level of obscurity.

What France sells: high exposure to sensitive geopolitical blocs

On the export side, the diagnosis is no more reassuring. In 2023, 20.64 % of French intermediate production was destined for foreign markets. And once again, the top foreign “client” is FIGW1 with 97.7 billion euros.

Other major clients include:

|

|

But the weight of geopolitically sensitive countries is striking:

🇺🇸United States: 47.17 billion euros

🇨🇳China: 33.18 billion euros

🇹🇷Turkey: 7.89 billion euros

🇷🇺Russia: 5.89 billion euros

🇸🇦Saudi Arabia: 1.88 billion euros

These dependencies are not only economic. They are political, technological, and strategic.

France’s strategic sectors rely on fragile value chains

Sector analysis reveals a major pattern: the sectors that carry France’s industrial sovereignty are also the sectors most exposed to international dependencies.

Most exposed sectors on the purchasing side:

Chemicals

Automotive

Metallurgy

Electronics

Machinery and equipment

Refined petroleum

Energy

Industrial food processing

Most exposed sectors on the sales side:

Aerospace and naval transport

Chemicals

Technology and electronics

Machine tools

Automotive

Defense and public administration

In other words: the sectors that matter the most are also the ones that would be hit the hardest by a geopolitical disruption. And yet, in terms of number of companies, these sectors are extremely small: only about 1200 to 1500 truly strategic companies across the entire country.

The resilience of France relies on them.

Dependencies on sanctioned countries: low in volume, critical in nature

Surprisingly, flows with officially sanctioned OFAC and EU countries are relatively small. Russia accounts for 4.34 billion euros in imports and 5.89 billion euros in exports.

At first glance, nothing alarming. But these flows affect very specific sectors:

metals

chemicals

machine tools

industrial food processing

construction

transport

pharmaceuticals

scientific research

These sectors are tiny in number of actors but central in French industrial value chains. What matters is not the size of the flow. It is the depth of the dependency and the strategic nature of the goods involved.

The systemic risk: the French economy depends on actors it cannot see

The global picture can be summarized as follows:

France depends on foreign actors for 20 to 25% of its ability to function.

A significant part of these dependencies is blurry, poorly documented, or invisible (FIGW1).

The most exposed sectors are also the most strategic.

French sovereignty relies on a very small number of industrial companies.

This is the definition of an unmanaged systemic risk.

France is not only dependent. It is dependent on actors it has not identified, in sectors it does not monitor, across value chains it cannot see beyond the first tier. No country is sovereign under these conditions.

Why this diagnosis matters: strategic sovereignty starts with visibility

France has the capacity to produce, export, and innovate. What it does not have, like all Western countries, is the ability to see its real dependencies. FIGARO provides a macro picture. SIRENE provides a surface-level structure.

But no state today has operational visibility into its value chains:

indirect suppliers

real countries of origin

multi-tier dependencies

geopolitical exposure

risk concentration

vulnerabilities linked to FIGW1

critical companies

potential points of failure

This is not an economic issue. This is a strategic sovereignty issue.

A state cannot protect what it cannot see.

A company cannot anticipate what it does not measure.

An economy cannot withstand what it does not understand.

For France, the first step is not to produce more. It is to make the invisible visible.

This is exactly what Sentinel is designed to achieve

It is not enough to know that 23 percent of purchases come from abroad. You need to know from whom, how, through which chain, through which intermediary, with which geopolitical risks, and with what probability of disruption.

Sentinel was designed for exactly this purpose:

reconstructing real value chains from public, private, and satellite data

automatically identifying critical dependencies

measuring exposure to geopolitical blocs

detecting breaking points across industrial chains

analyzing multi-tier suppliers

assigning sector and national sovereignty scores

allowing decision-makers to see what was previously invisible

Strategic sovereignty is not a slogan. It is an operational capability built on knowledge.

And knowledge starts with one thing: visibility.

In conclusion

This analysis does not tell a story about international trade.

It tells the story of France’s deep dependencies, the ones that define its ability to produce, invest, defend itself, and innovate.

The diagnosis is clear: France depends far more than it believes, and more importantly, it depends on actors it cannot see.

In a world where geopolitics reshapes economic rules, the real question is no longer “How much do we depend on?” but “Are we able to see our dependencies before they turn into ruptures?”

With our Sentinel solution, the answer can finally be yes.

Every week we publish the analysis of a new country on this blog. Sign up for free here.